What is the Significance of the Author s Continued Emphasis on Segouin s Wealth

Investment Thesis

Manulife Financial Corporation (NYSE:MFC) has achieved a total return of ~30% since I last recommended the company in January 2019. In that analysis: "Manulife Is Looking Like A Promising Turnaround Story " I outlined the company's business fundamentals and associated valuation. This article will focus on the opportunity Manulife has to continue expanding its business in Asia. The rise of the Asian middle class represents a compelling growth opportunity for Manulife to expand its insurance and wealth management operations in a region with strong demographic tailwinds. With a vast footprint and a long history in Asian markets, Manulife is well positioned to continue the expansion of its Asian business, while maintaining its core North American insurance business. This strategy will continue to support Manulife's commitment to rewarding shareholders with dividend growth and share repurchases over the long-term. With Manulife's strong position and growth potential, it is an ideal long-term holding for dividend growth investors.

Source: Financial Post

Company Profile

Trading as "MFC" on the Toronto Stock Exchange, New York Stock Exchange, and under '945' on the Stock Exchange of Hong Kong, Manulife Financial is a leading financial services company meeting the investment and insurance needs of 28 million customers around the world. Over the last 131 years, Manulife has grown to become one of the top ten global insurers with CAD $1.2T in assets under management and administration. With 34,000 employees globally, Manulife operates Wealth and Asset Management services and runs comprehensive insurance businesses in Canada and Asia as Manulife; and in the U.S. under its brand John Hancock. Manulife took heavy losses in the global financial crisis last decade and has spent much of the last 10 years rebuilding its balance sheet and optimizing its portfolio of business. With a strengthened balance sheet and robust capitalization, the company's global diversification has allowed it to leverage the stable cash flows of its North American business to grow its footprint in its key growth markets in Asia.

Source: Manulife Corporate Fact Sheet

The Asian Opportunity

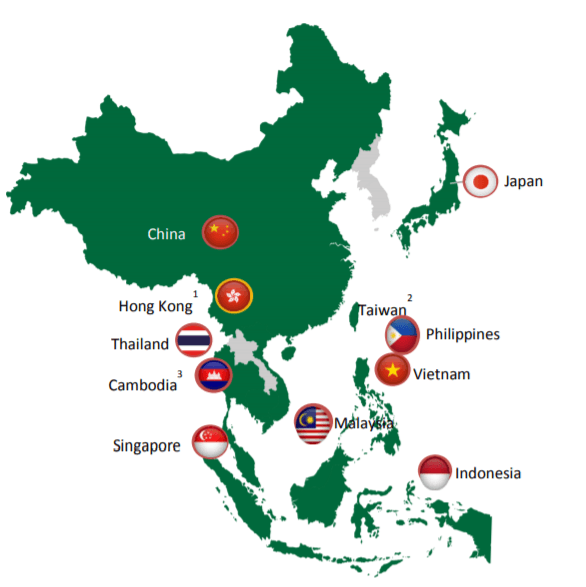

Manulife has operated in Asia since 1897 when it opened its first Asian office in Shanghai more than 120 years ago. It expanded into Hong Kong, Singapore and Japan in the following decade. In the Philippines, Malaysia and Indonesia, Manulife has been providing financial services for over 100 years. In more recent decades, the company has built and acquired businesses opening up markets in Taiwan, Vietnam and Cambodia. Through the division's 11,000 employees and network of 70,000 contracted agents, Manulife provides financial services to over 10 million customers in Asia. Manulife also has over 100 bank partnerships with firms across Asia, providing access to over 14 million banking customers. The company offers: individual life insurance, group life and health, hospital coverage, wealth preservation, mutual funds, pensions, annuities and investment-linked products across its Asian markets.

Source: Manulife Asia Factsheet

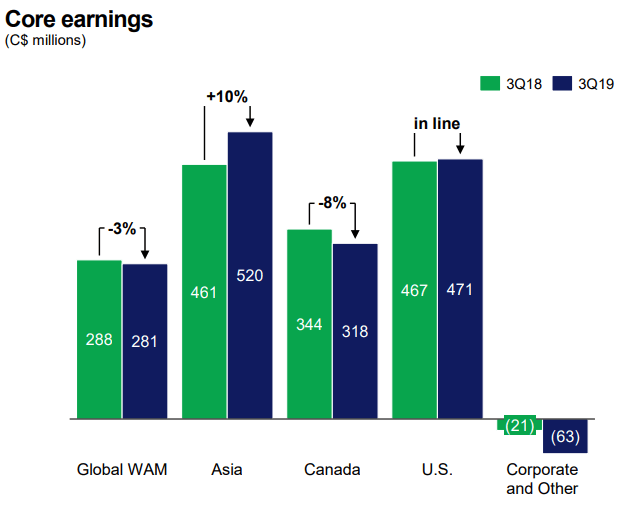

In 2018, Manulife's Asian segment contributed 29% of the company's core earnings and accounted for 10% of the firm's assets under management and administration. From 2017 to 2018, core earnings in Manulife's Asian operations grew by an impressive 20%. Net income attributable to shareholders doubled from CAD $818M in 2016 to CAD $1.687B in 2018. This growth trend has continued into 2019 with core earnings in Q3 2019 up 10% year over year. In the 3rd quarter of 2019, Manulife reported CAD $71M in core earnings in its Asian Wealth Asset Management division, up from CAD $65M in 2018. To ensure that the company's leadership is well prepared to continue advancing its growth opportunity in Asia, Manulife promoted Roy Gori to CEO in 2017, having led Manulife's Asian division since 2015.

Source: Manulife Investor Presentation

Growth Strategy

While Manulife has made a number of acquisitions in Asia including its notable purchase of Standard Chartered PLC's (OTCPK:SCBFF) pension business in 2015, the firm has largely focused on growth with strategic partnerships. Manulife has signed exclusive agreements with several regional banks to be their sole provider of insurance products. Deals with DBS Group Holdings Ltd (OTCPK:DBSDF) and Standard Chartered have given Manulife exclusive access to these banking clients out to 2030. Manulife has employed a similar strategy as it entered into the Indian wealth management market through the formation of a joint venture with Mahindra & Mahindra (OTCPK:MAHDY) in which Mahindra will have a 51% stake. This joint venture allows Manulife to de-risk its entry into this massive market and take advantage of Mahrinda's domestic strength while leveraging Manulife's global wealth management capabilities.

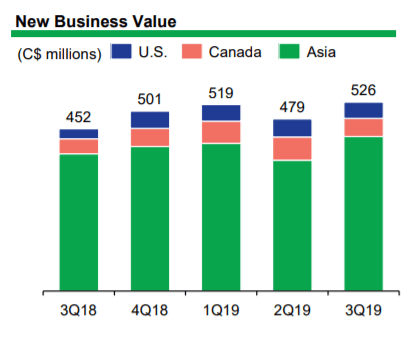

During Manulife's Q2 2019 earnings call, the company's executive spoke to the firm's intentions towards organic growth vs acquisitions. CEO Roy Gori reiterated that the company has confidence in its ability to continue meaningful organic growth without having to pursue acquisitions. While Manulife continues to look at acquisitions opportunities strategically, the firm sees better value in deploying capital to share repurchases. This signals to investors that the firm sees its current share price as relatively inexpensive and that the company is confident that its current growth model is working. This strategic discretion regarding acquisition opportunities was evidenced when on November 17th Bloomberg reported that Manulife is competing to buy Aviva Plc.'s (OTCPK:AIVAF) Asian assets. Aviva has since decided not to sell its Singapore or Chinese assets, likely due to the low bids made by Manulife and others. Aviva is still advancing the sale of its Vietnamese, Hong Kong and Indonesian assets which may be a great complement to Manulife's large portfolio of Asian assets. These strategies have been successful for Manulife as it continues to grow its new business value in Asia at an impressive rate.

Source: Manulife Q3 2019 Results Fact Sheet

Asian Market Demographics

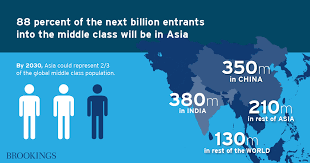

The world is currently undergoing an unprecedented expansion of the middle class; particularly in Asia. According to the Brookings Institution, 880 million of the next one billion entrants to the global middle class will come from Asia. 160 million people will join the global middle class each year, the majority of them in the Asia-Pacific region. By 2030, Asia will represent 2/3 of the world's middle class with at least 2.8 billion middle class Asians by 2025. As a result of this demographic paradigm shift, net household wealth in Asia is expected to grow at an annualized rate of 16.4% compared to North America's rate of 6.4%. By 2030 Asia is projected to account for 66% of the global middle-class population, compared to 28% and in 2009.

Source: Brookings Institution

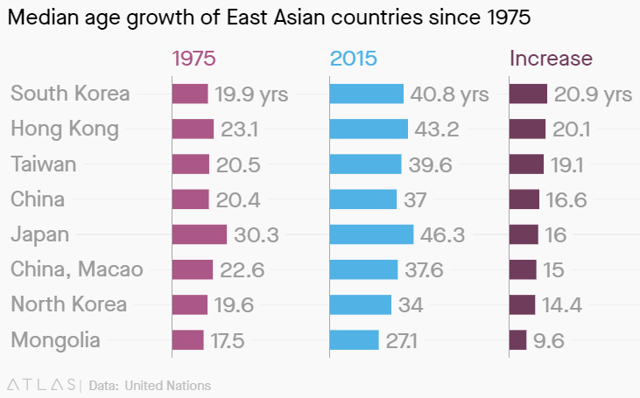

With Manulife operating in 12 distinct Asian markets, there is significant diversification within the vast Asian market segment. Manulife has operations in mature markets such as Japan as well as developed markets like Hong Kong and Singapore and in developing ones such as Vietnam and Indonesia. This mix of developed and emerging economies is characterized by different demographics. The developing nations of the Philippines and Vietnam have a much younger median age than the advanced economies of Japan, Hong Kong and Taiwan. One thing these countries all have in common though is that they are all aging. Asia-Pacific is among the fastest aging region of the world.

Source: Quartz

Manulife has an opportunity to significantly grow life insurance sales in the underpenetrated emerging economies of Asia while simultaneously focusing on health insurance and wealth management for the aging populations of the developed economies of Asia. As household wealth tends to grow as individuals age, the aging population of the entire Asia-Pacific region represents a very attractive market for Manulife's Wealth and Asset Management division. The demographic diversification across these 12 jurisdictions helps to smooth out earnings and mitigate the impact of any regional economic challenges or geographic/political risks.

Health Insurance

With the population of Asia aging, growing wealthier and increasingly urban, the need for health insurance is set to expand dramatically. State run insurance providers will be supplanted by private coverage and health expenses will continue to outgrow income. Aging urban dwellers in country's where life expectancy will continue to grow will see increasing costs for elder care and health care. According to Ernst and Young's Asia-Pacific Insurance Outlook 2019, health insurance is the "Torchbearer of growth" in Asia:

Health insurers will get a strong push from the development of private healthcare ecosystems. Historically, insurers have looked to buy hospitals and other assets in building these ecosystems. In the future, they will position themselves at the center of ecosystems to promote better customer experiences and value propositions more relevant to customers.

To capitalize on these trends, Manulife has entered into a strategic partnership with a major healthcare platform in China to offer insurance as well as launched ManulifeMOVE in Singapore Hong Kong and mainland China. This program which doubled enrolment in 2018, encourages active living and offers discounted premiums for healthy activities.

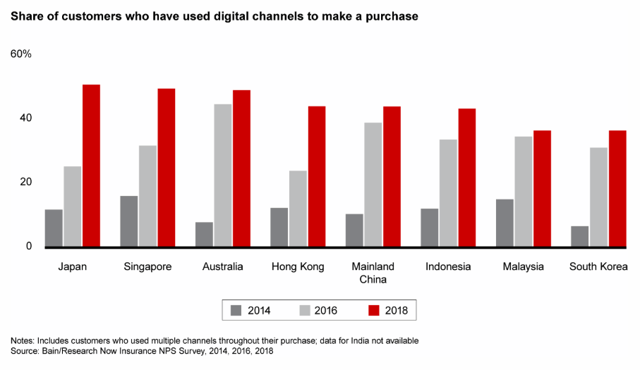

Digital Opportunities and Efficiency

In Manulife's 2018 Annual Report, CEO Roy Gori highlighted five key priorities for the firm, one of these was to focus on digital leadership. Consumers are buying more insurance online which requires that insurers enhance their digital platforms in order to stay relevant and competitive. According to Bain & Company

The insurance distribution landscape is changing. In life insurance, traditional channels remain dominant in mature markets such as Australia, Hong Kong, Singapore and Japan, but in developing markets such as mainland China, India, Malaysia and Indonesia, digital channels are becoming more prominent.

Source: Bain & Co

In response to these digital trends, Manulife launched a number of initiatives over the last two years including: the introduction of facial recognition that allows real-time verification for policy holders in China and the launch of a new eClaims service in Hong Kong, Japan and Vietnam to simplify the claim submission process. In Japan, Manulife has rolled out a new electronic point-of-sale system designed to promote additional product offerings and focus on customer preferences.

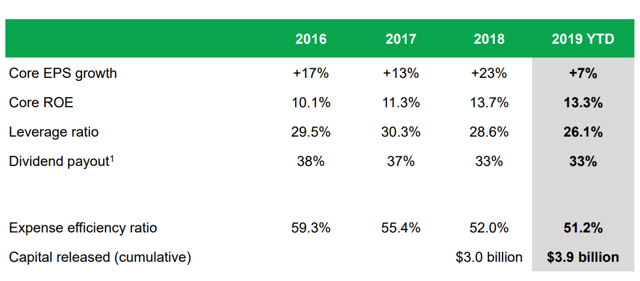

Not only have these initiatives served Manulife to better meet the needs of its customers, they also contribute to the lowering of the firm's overall cost structure. Insurance is a competitive industry and cost controls are important for long-term profitability. Optimization initiatives such as enhanced digital offerings have contributed to the firm lowering its overall efficiency ratio by over 8% since 2016. In 2018, Manulife set a target to reduce expenses by $1B by 2022 through a series of targeted initiatives. Manulife's management team has done an admirable job of this as expense growth has continued to slow in recent quarters.

Source: Manulife Investor Presentation

Dividend & Share Repurchases

I like opportunities to buy Canadian listed companies that qualify for the Canadian dividend tax credit where a significant portion of revenues come from outside of Canada. Between the firm's Wealth and Insurance businesses, 73% of Q3 2019 revenue was derived outside of Canada. A globally diversified business such as Manulife offers the opportunity to diversify from Canadian economic conditions while maintaining the domestic tax benefits of favourable dividend tax treatment.

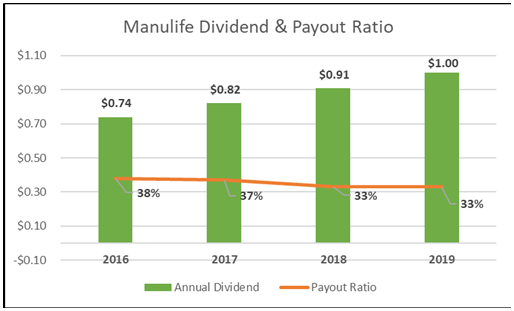

As a long-term dividend growth investor, I favour companies that can achieve regular dividend increases while simultaneously decreasing or stabilizing their payout ratios. This is a confidence signal that portends sustainable dividend growth over the long term. Over the last few years, Manulife has offered investors steady dividend increases all while reducing the company's payout to the lower end of its 30-40% target range.

Source: Author

Shares of Manulife are currently yielding 3.9% with a quarterly pay out of CAD $0.25. Over the past 5 years, Manulife has achieved a dividend CAGR of 12%, including a 13.6% increase in 2018. This record of dividend increases has been fueled by stable earnings in Canada and the U.S. and growth in Asia. As Manulife continues to build out its Asian business, it should be able to continue rewarding shareholders with dividend growth over the long-term.

In the company's most recent results, the firm reported a Life Insurance Capital Adequacy Test (LICAT) Ratio of 146%, up from 134% the year prior. This balance sheet measure is a result of Manulife having CAD $26B more in capital than it is required to have by regulators. As this measure equates to more capital than the firm expects to have, the company is in a position to allocate additional capital to rewarding shareholders. In addition to dividend increases and debt redemptions, Manulife will also take the opportunity to buy back shares.

On November 12, 2019 Manulife announced that the firm has received approval from the TSX to pursue its previously announced NCIB permitting the firm to repurchase up to 58 million shares or about 3% of Manulife's outstanding common shares over the next 12 months. This share buy back will boost EPS as well as serve to assuage concerns about the need to raise additional capital.

Valuation

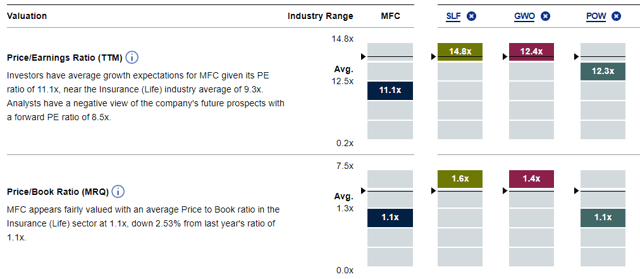

Manulife has had a positive year, with shares on the TSX up approximately 18% over the last 12 months. As a result, the current share price is certainly closer to the company's fair market value. When compared to the other Canadian insurance companies, Manulife trades at a lower P/E and P/B ratio than the comparator average.

Source: RBC Direct Investing

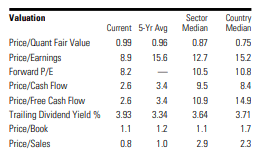

When looking at Manulife from a historical valuation perspective, it is still undervalued despite the recent run-up. At approximately CAD $26, Manulife is currently trading at a 1.1X book value, slightly below the company's long term average of 1.2X book value. On a price to earnings basis, Manulife looks reasonably priced, trading at 8.9X, compared to the firm's 5-year average of 15.6X.

Source: Morningstar

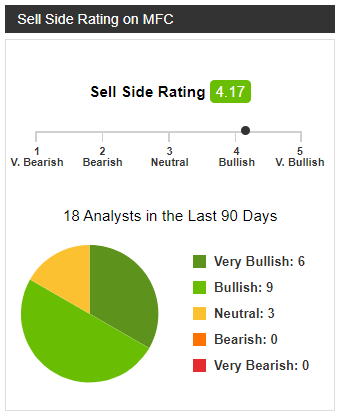

According to Ryan Bushell, President of Newhaven Asset Management Manulife has had a good run up and should continue to rate higher compared to its peers. Bushell suggests that future acquisitions and assets sales could be catalysts for additional share price appreciation. While the analyst sentiment is very positive, Manulife is now trading at 1.1X its book value, slightly below its 5-year average of 1.2X. In the coming months, the firm could reasonably revert to its mean 1.2X book valuation offering a 9% upside to the current share price. This coupled with the 3.9% dividend yield offers an attractive total return opportunity of approximately 12-13%.

Source: Seeking Alpha

Risk Analysis

One of the inherent risks associated with investments in insurers is the associated exposure to interest rate risk. Manulife has endured persistently low interest rates in jurisdictions such as the U.S and Canada. While the company would stand to gain tremendously if interest rates rose, the company is also exposed to interest rate decreases and prolonged low interest rate environments.

With significant operations in Hong Kong, Manulife could potentially be impacted by an economic slow down in the territory as a result of the recent political protests. In the Q3 2019 earnings call, Phil Witherington, Manulife's Chief Financial Officer assuaged concerns about disruptions by sharing that mainland Chinese visitors to Hong Kong represent a modest component of the company's business in Hong Kong and accounted for only 14% of APE sales in Q3 2019, and 18% in full year 2018.

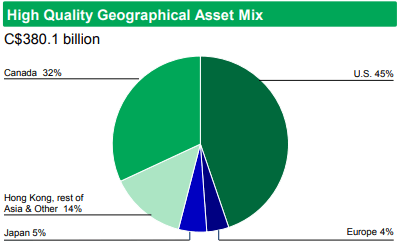

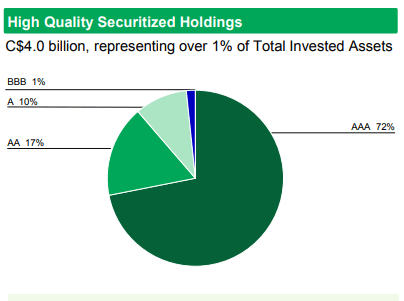

In addition to this political/geographic risk, Manulife also carries notable economic risks. The firm makes money by investing the proceeds of its insurance premiums into a portfolio of global investments. As occurred in 2009, Manulife would be negatively impacted by a sharp crash in the financial markets. That said, the firm is better prepared today than it was in 2009 to weather an economic downturn. According to Rajiv Bhatia, Equity Analyst at Morningstar, less than 2% of Manulife's bond portfolio is exposed to BB rated or lower securities, while 75% is invested in A to AAA rated securities. This high quality asset mix has helped to de-risk the portfolio and better prepare the company to endure future market volatility.

Source: Manulife Corporate Fact Sheet

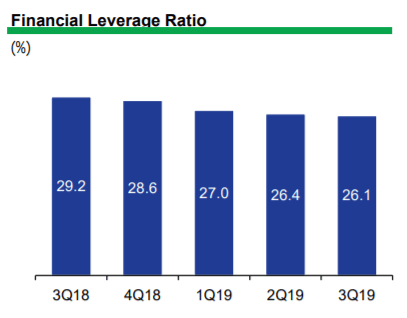

Manulife has done a commendable job of strengthening its balance sheet in recent quarters improving its financial leverage ratio from 29.2% in Q3 2018 to 26.1% in Q3 2019.

Source: Manulife Q3 2019 Results Fact Sheet

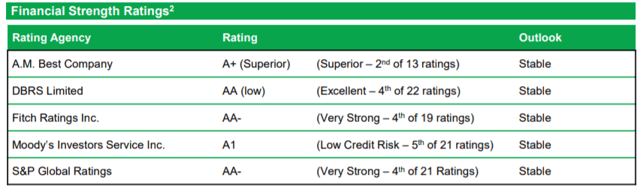

From a financial strength perspective, Manulife has maintained investment grade credit ratings by staying well capitalized. Manulife boasts some of the highest credit ratings available for ratings agencies with an unanimously stable outlook.

Source: Manulife Q3 2019 Results Fact Sheet

Investor Takeaways

With a strong foothold in a dozen Asian markets, Manulife is well positioned to continue benefiting from the positive trends in Asia. Manulife is growing life insurance sales in the underpenetrated emerging economies of Asia while simultaneously focusing on health insurance and wealth management for the aging populations of the developed economies of Asia. By capitalizing on the immutable demographic trends in a region experiencing unprecedented economic growth Manulife will continue to grow core earnings. This visibility towards continued long-term growth gives management the free cash flow availability and confidence to continue rewarding long-term shareholders through dividend increases and share repurchases. Manulife is an ideal long-term holding that offers high quality, share price up-side and dividend growth.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

This article was written by

I am a value-oriented investor who seeks out high-quality companies with long histories of dividend growth. I believe that patient investors who build a core portfolio of dividend paying equities can achieve their retirement goals without taking on unnecessary risk. Dividend growth profiles are the best indicators of management's commitment to returning cash to shareholders. Dividend growth investing involves identifying quality companies with competitive advantages that provide visibility towards future cash flow growth. Warren Buffet once wrote "If you don't find a way to make money while you rest, you will work until you die". Fundamental analysis and patience are the tools I use to build a portfolio of equities that will enable my very comfortable retirement. Join me in exploring value and growth-at-a-reasonable-price opportunities and in building your own income-producing portfolio of dividend stocks. I am an investor with over 20 year of experience in the market. I hold a B.Mgt and an MBA where I enjoyed studying both corporate and personal finance.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Source: https://seekingalpha.com/article/4309554-manulife-for-long-term-growth-in-asia-will-continue-driving-core-earnings-growth

0 Response to "What is the Significance of the Author s Continued Emphasis on Segouin s Wealth"

إرسال تعليق